Let's start from the beginning. Can a country that seemed doomed to a hyperinflationary crisis, with a semi-defaulted debt and a nearly bankrupt Central Bank transform in two years into a coveted piece for the world's major investors? It can, but not by chance. With a tornado sweeping away bureaucracy, unproductive public spending, and unprecedented laws for an oxidized Argentina, it is becoming possible.

Perhaps, the magnitude of the change is hard to appreciate from up close, but it does not go unnoticed by a world that is stiff and eager for business opportunities. And, as without “risks there are no profits,” everything that has played in favor so far, and that consolidates for the remainder of this promising 2026, has an inevitable negative side implicit in the doubt of a relatively near future: will Argentines want to continue betting on growth and sustained progress in 2027 while accepting the challenges that come with embracing market rules and letting go of the false illusions of protection from a state that is almost never there when they really need it?

There lies probably the greatest dilemma of the sustainability of this new model, which does not raise doubts in the long term but imposes challenges in the immediate term. Making the change feasible also implies resigning some of the deeply rooted egalitarian gene of being Argentine, which positioned us discursively as a progressive society in the last century, but mercilessly condemned us to stagnation that systematically resigned growth opportunities to most of our Latin American neighbors.

Let's take a quick look at these two years of government. The first thing Javier Milei did was to set up a consistent and credible fiscal, exchange rate, and monetary stabilization plan that achieved quite immediate results: monthly inflation dropped from 25% to 2.5%, the fiscal surplus crystallized very quickly with a brutal reduction of public spending close to 30%, and the exchange rate managed to remain at fairly stable values in real terms, even after the lifting of the capital controls and despite the most brutal dollarization of portfolios in Argentine history between June and October 2025, close to 50% of the money supply and bank deposits.

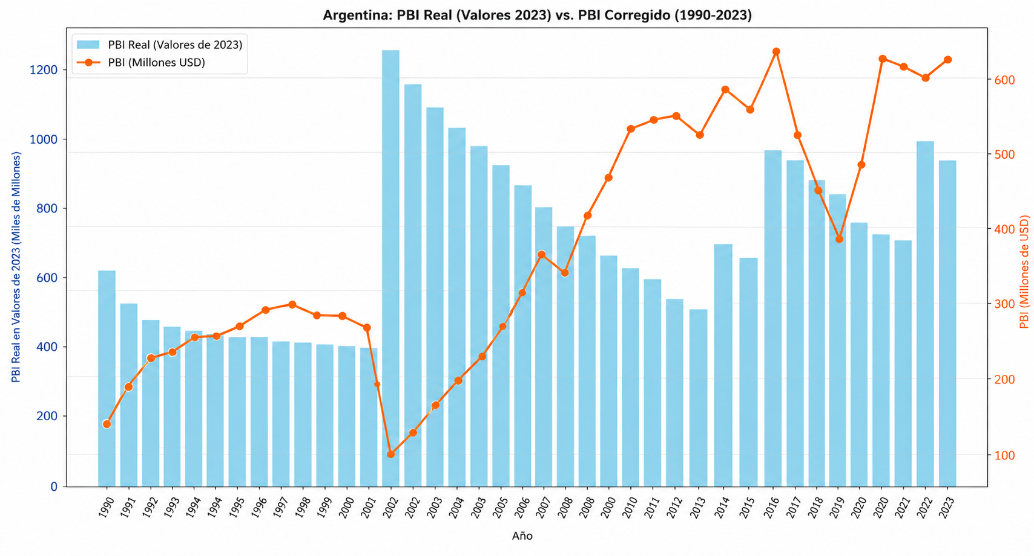

Ah, but then, surely he did it by “manipulating” the dollar and sacrificing both competitiveness and economic activity. Let's see what AI tells us about this for the last 30 years:

It not only seems that when the exchange rate stabilizes, production grows, but also that we are not even close to a low real exchange rate today. Averaging an exchange rate during times of capital controls with another in years of freedom to calculate a supposed dollar more representative of the last decades is a fallacy that statistical science can afford but not responsible economic science.

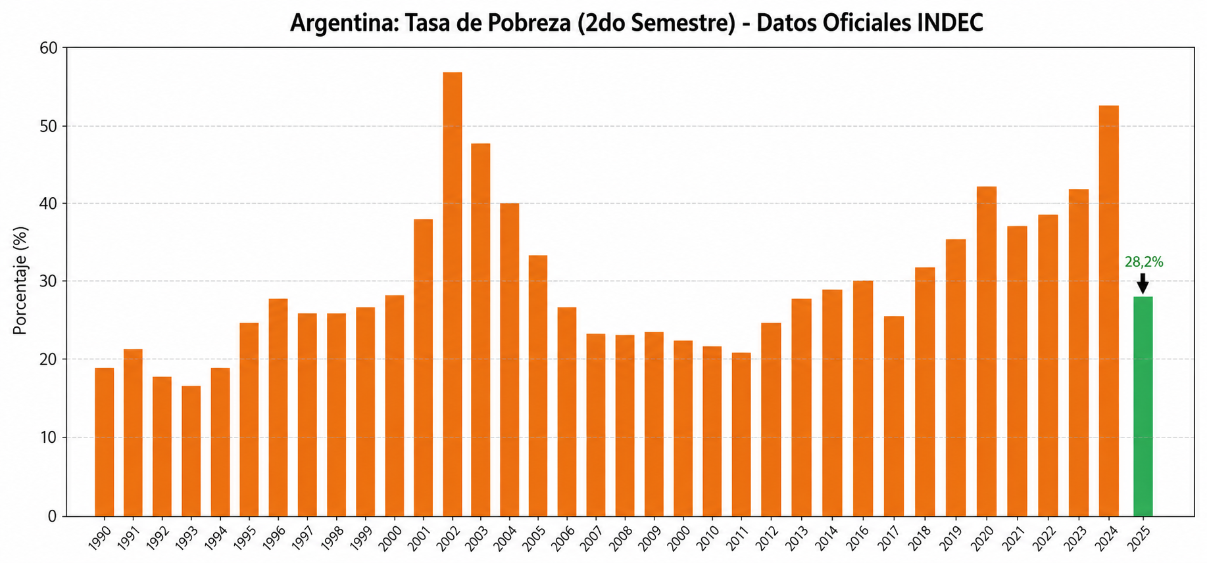

Quickly, the horsemen of the apocalypse will come to tell us that perhaps this new model does not paralyze economic activity, but concentrates it in a few dynamic and privileged sectors, expelling a large number of people into poverty and indigence.

We asked AI about this again, and this is what it reproduced based on the official data from the National Institute of Statistics and Censuses:

Far from it, in these two years the poverty rate measured in the same way as decades ago has decreased significantly. A good part of this decrease is explained because macro stabilization facilitated that food prices grew well below general inflation and due to a very efficient social policy, both in terms of the monetary value secured and in the elimination of “bureaucracies in social movements,” which drained a good part of the resources that should have been directed directly to vulnerable people.

Now, was a successful stabilization process enough to transform the expectations of a country that had spent two decades ruining its reputation regarding compliance with its commitments and respect for private property?